If you have been pricing up a new handset, the numbers behind phone prices in 2026 are about to get uncomfortable, and the cause has almost nothing to do with the phone itself. The squeeze starts in the memory chips, where an AI building boom has drained the supply that smartphones rely on. TrendForce reported in January 2026 that memory makers are prioritising server customers, driving across-the-board price rises into the first quarter, and the effect is now feeding through to the devices on the shelf at Currys and in the EE store.

- Counterpoint Research, reported by CNBC on 16 December 2025, expects the average smartphone selling price to rise around 6.9% in 2026, up from an earlier 3.6% estimate.

- Counterpoint’s March 2026 memory tracker puts the hit at roughly $30 on budget phones and $150 to $200 on premium handsets.

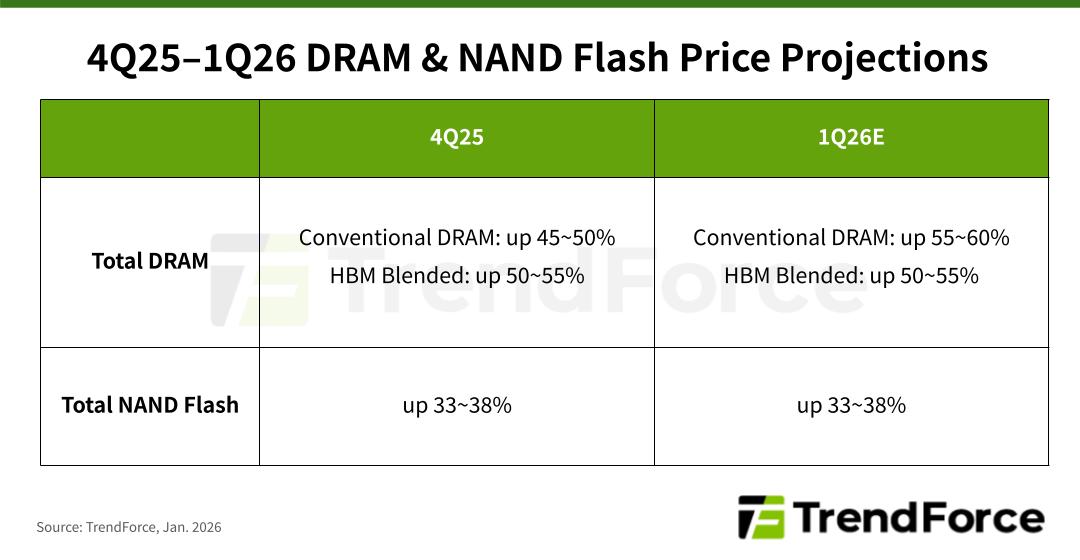

- TrendForce forecasts conventional DRAM contract prices climbing about 63% quarter on quarter in Q2 2026, with NAND flash up to 75%, after near-95% jumps in Q1.

- Why it matters for you: the rise is structural, not a temporary blip, so the timing of your next upgrade now carries a real cost.

Where the cost increase actually starts (memory-price squeeze)

The story begins in the data centre, not the phone shop. Training and running large AI models needs vast quantities of high-bandwidth memory, and the firms that make DRAM and NAND flash, principally Samsung, SK Hynix and Micron, have steered their output towards the server customers who pay the most. TrendForce projected on 22 January 2026 that the memory market would be worth $551.6 billion in 2026 and surge towards $842.7 billion in 2027, growth of more than 50% driven by cloud providers expanding AI infrastructure.

When a factory line can sell the same wafer to a hyperscaler at a premium, the chips left for consumer devices get scarcer and dearer. That is the mechanism, and it is worth understanding before you read a single rumour about a flagship price. The same memory crunch that is pushing up the cost of a desktop RAM upgrade is the one nudging your handset bill higher. If you are weighing whether to hold your current phone, our guide on whether to skip the 2026 upgrade and buy last year’s flagship sits directly on top of this question.

Samsung sits at an unusual pinch point in all this. It is one of the three companies that make the memory the whole industry needs, and it is also one of the biggest phone makers buying that memory back for its own handsets. When its memory division can earn more selling to AI server builders, its mobile division faces the same rising bill of materials as everyone else. That tension is why even a vertically integrated giant cannot fully shield buyers from phone prices in 2026.

How memory feeds into a phone’s retail tag

A phone’s price is built from its bill of materials, the parts list, plus assembly, marketing, tax and margin. Memory has quietly become one of the largest single line items on that list. Counterpoint Research, in analysis dated 11 March 2026, found that on a premium phone with 16GB of LPDDR5X RAM and 512GB of storage, RAM accounts for around 23% of the bill of materials and storage another 18%. On a low-end phone, memory can be as much as 43% of the total.

Senior analyst Shenghao Bai noted that mobile RAM had risen roughly 50% quarter on quarter while NAND storage had climbed more than 90%. When two-fifths of a budget phone’s parts cost suddenly jumps by a quarter, the maker has three choices: absorb it and lose margin, cut features, or raise the price. Most will raise the price. This is the same logic that runs through our look at whether the Galaxy S26 is worth it in the UK, where the spec sheet alone no longer tells the value story.

Counterpoint’s headline figure, reported by CNBC on 16 December 2025, is that the average selling price across the whole market could rise about 6.9% in 2026, well above its earlier 3.6% forecast. That is an average; the spread matters more. The same research puts the increase at roughly $30 on a cheap phone but $150 to $200 on a flagship, because premium devices carry far more memory. The pound has its own part to play here too, since UK prices already bake in VAT and exchange-rate cushioning that US sticker prices do not.

The base-storage decision nobody talks about

There is a second, sneakier effect. Makers can hold a headline price steady while quietly changing what you get for it, and storage is the easiest lever to pull. Industry chatter through 2026 has pointed to Google dropping the 128GB option and moving the Pixel 11 line, the Pro tier in particular, to a 256GB starting point. Treat that as a rumour for now, not a confirmed spec, but it is a plausible one: if 128GB and 256GB tiers cost almost the same to stock during a NAND shortage, consolidating on the larger size simplifies the supply chain.

The reader-facing consequence is subtle. A 256GB base sounds generous, and for many people it is genuinely useful, but it also raises the floor price of the cheapest model in a line. You lose the option to buy in at a lower storage tier even if 128GB would have done you fine. For the full rumour picture on Google’s next phone, our Pixel 11 leaks round-up tracks the storage and modem talk, and our Android 17 guide for UK Pixel owners covers what the software side adds.

The price tag can stay still while the cheapest version you are allowed to buy quietly gets more expensive.

Foldables are the other pressure point. They already command a premium, and persistent rumours suggest 2026 foldable pricing will edge up further. Again, label that as unconfirmed until a maker publishes a UK recommended retail price. The principle holds regardless: the more memory a device packs, the more exposed it is to this squeeze, and foldables and Ultra-tier phones pack the most.

Who is most exposed, and who can ride it out

Not every maker is equally exposed. The three memory producers, Samsung, SK Hynix and Micron, hold some insulation because they make the component in-house, though Samsung still competes for its own scarce supply. Apple has the scale and margin to absorb a chunk of the increase if it chooses, and a habit of holding nominal prices while adjusting configurations. Smaller brands that buy all their memory on the open market have the least room to manoeuvre and may pass the most through.

That uneven exposure changes the value map. A budget phone where memory is 43% of the parts cost feels the percentage rise hardest, which is why the cheapest end of the market may see the sharpest relative jumps even though the absolute pound figure is small. If you are shopping at the affordable end, our take on the Pixel 10a at £499 and the sub-£600 iPhone 16e versus Nothing Phone 4a contest are worth reading before you commit, because last year’s pricing may not survive into the next refresh.

Shipment forecasts tell their own story. Counterpoint expects global smartphone shipments to fall about 2.1% in 2026, a sign that makers anticipate higher prices cooling demand. A shrinking market with rising costs is a recipe for fewer, pricier choices rather than the usual flood of cheap options. That is the backdrop against which every 2026 launch should be read.

Buy now or wait: the timing maths for UK buyers

Here is where it gets practical. Because the memory rise is structural and forecast to deepen through Q2 2026, the usual advice to wait for the next model is weaker than normal. Waiting often means waiting for a more expensive model. If your current phone is failing and you can buy a current-generation device at today’s UK price, there is a real argument for moving now rather than betting on a cheaper future. Amazon’s mid-year sale is one window worth watching, and our Prime Day 2026 fake-discount guide explains how to tell a genuine cut from an inflated one.

The contract-versus-SIM-free question gains a new wrinkle too. A SIM-free purchase locks in today’s handset price in one payment, insulating you from future rises on that specific device. A contract spreads the cost but exposes you to mid-contract increases, which since Ofcom’s January 2025 rules must now be shown in pounds and pence rather than as a CPI percentage. Uswitch’s 2026 guidance notes EE and O2 customers facing rises of up to £2.50 a month from spring 2026. Our explainer on mid-contract price rises and your Ofcom rights sets out exactly what you can and cannot be charged.

If you do decide to upgrade, the comparison work matters more than ever when every pound counts. Our head-to-head on the Pixel 10 versus iPhone 17 at £799 and the question of whether to buy the iPhone 17 now or wait for Prime Day both apply the timing logic above to specific handsets you can actually order today.

My verdict

My view is that 2026 is the year the old upgrade reflex stops paying off. The memory squeeze is real, sourced and structural, not a marketing scare: TrendForce and Counterpoint both describe a multi-quarter rise driven by AI server demand, and it is already in the bill of materials behind the phones you can buy. I would not panic-buy, but I would stop assuming that waiting saves money, because in this cycle it often does the opposite. If your phone still does the job, hold it and skip a generation; the longer you keep a working handset, the more this whole squeeze passes you by. If you genuinely need a new device, buy a current-generation model at today’s UK price from a retailer with a clear returns window, favour SIM-free to lock the cost, and treat any unconfirmed flagship price you read as a rumour until a maker publishes a UK figure. What would change my advice is a sudden easing in DRAM and NAND contract prices, and right now the forecasts point the other way.

Phone prices in 2026: frequently asked questions

Related reading on MTW

- Skip the 2026 upgrade: buy last year’s flagship and pocket the difference

- Pixel 10 vs iPhone 17: which £799 flagship wins in the UK

- UK mid-contract price rises in 2026: your Ofcom rights explained

MMTW Editorial

Buyer action

Where to buy or check next

Use this as the final check before ordering a phone, changing network or trusting a headline monthly price.

Reader discussion

Leave a comment

Comments are moderated. Keep it useful, accurate, and on topic.